SCM Direct · Market Insight

Why a rush of mega-IPOs is a passive problem, not yours

A client wrote to us recently, worried about two developments being reported in the papers: the relaxation of index-inclusion rules just as a queue of very large, very thinly floated listings builds behind SpaceX, and the murkier world of “tokenised” share listings.

The concerns are well-founded – but they fall overwhelmingly on the conventional, cap-weighted passive investor. Here are why our portfolios are built to sidestep them.

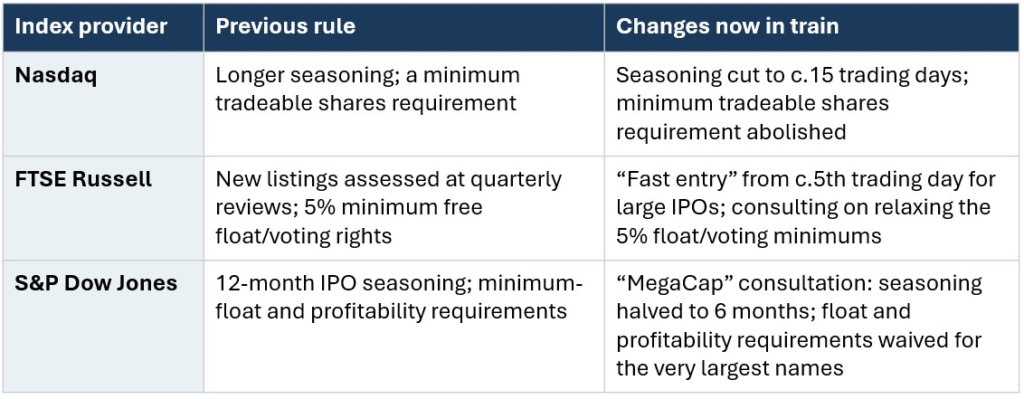

The rule changes – the reading is correct

The major index providers have been clearing a path for these mega-cap listings:

SpaceX could be forced into the big cap-weighted benchmarks quickly, on a float of only around 4–5%, at whatever price the post-IPO scramble produces. As one ETF strategist put it: “if SpaceX is up 100% the week after the IPO, and they have to buy it, they have to buy it… they can’t discriminate.” That is exactly the mechanism to worry about — and it is real. Katie Martin’s FT piece on market “enshittification” makes the wider point well.

How the ETFs we invest in avoid the bubble

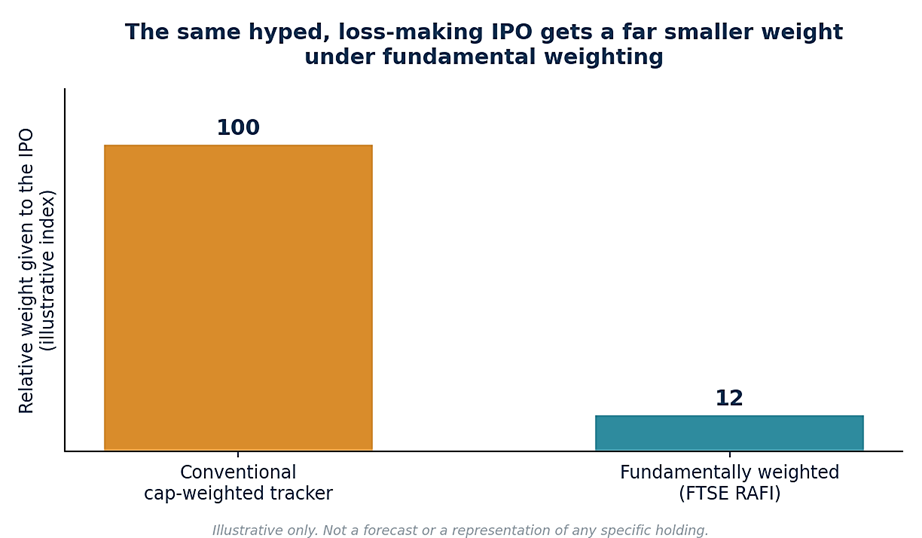

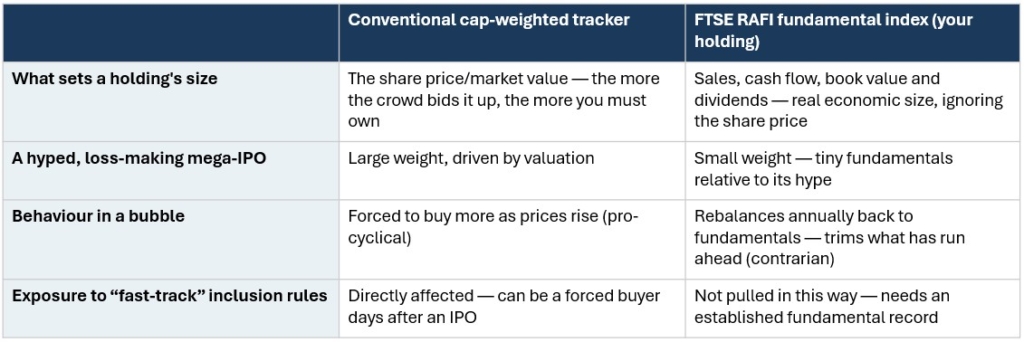

Our US exposure (save ethical portfolios) is achieved through the Invesco FTSE RAFI US 1000 UCITS ETF, which is fundamentally weighted rather than market-cap weighted. A conventional tracker holds each company in proportion to its market value, so the more the crowd bids a stock up, the more it is forced to own. The RAFI index ignores the share price and weights companies by four measures of real economic size: sales, cash flow, book value and dividends (plus buybacks).

The practical consequence for SpaceX is striking. It is reportedly coming to market at around 100 times revenue, lost roughly $4.9bn last year, and pays no dividend. On the measures that drive the RAFI index, it is a small company, so its weighting would be a tiny fraction of what it would command in a cap-weighted index. We are simply not a forced buyer of it at an inflated price.

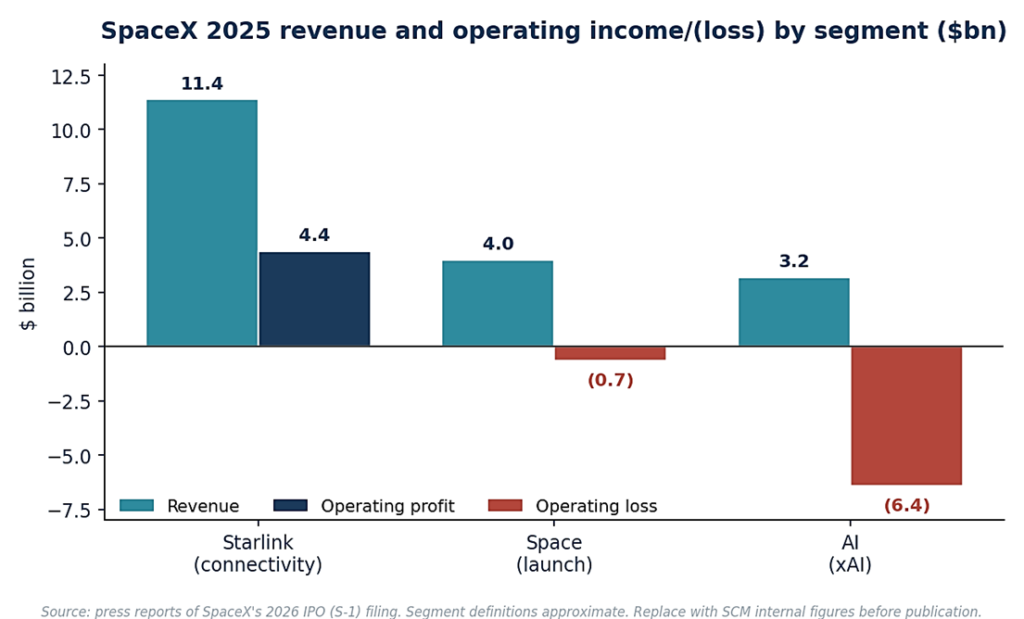

SpaceX 2025 revenue and operating income/(loss) by segment ($bn). Most of the group’s profit comes from a single engine — Starlink — while the Space and AI segments lose money. Source: press reports of SpaceX’s 2026 IPO (S-1) filing.

Two further protections apply.

First, the RAFI methodology is inherently contrarian: it reconstitutes annually back to fundamental weights, trimming holdings whose prices have run ahead and topping up those that have lagged; the opposite of a momentum-chasing tracker.

Second, the fast-track inclusion rules apply to the cap-weighted benchmarks, not to how a fundamental index admits names: a brand-new listing with no record on sales, cash flow, book value and dividends is not pulled in days after floating.

For all our clients (save those in the 100% Equity portfolio), there is a second line of defence: an active, risk-managed asset-allocation overlay.

We are not obliged to be fully invested in equities, so if markets turn as volatile as many expect, we have the latitude to hold more cash and lower-risk assets.

Will this wave of IPOs sink the market? SCM’s view: not yet, but watch 2027–28

A broader worry we hear is this: if SpaceX, Anthropic, OpenAI and others all come to market, with Alphabet alone planning to raise some $80bn, won’t that flood of new stock drag the whole market down? Bloomberg’s John Authers has set out the clearest framework for thinking about it, and his answer, which we share, is: probably not immediately, but the risk builds with time.

The reassuring part is context. This new issuance arrives after years of “de-equitisation”, a term coined by Citi’s Rob Buckland in 2003 for the steady shrinking of public equity. Buybacks, dividends, and cash takeovers have retired more stock than new listings have created, in effect, every year since then.

Goldman Sachs notes IPO activity has been in steady decline since the 2021 post-pandemic burst, and the S&P 500’s share count has been falling since 2003. As one commentator, Nir Kaissar, puts it, companies are now “not supposed to show up on exchanges already the world’s most valuable businesses” – yet that is exactly what is about to happen. The slivers the new AI and space giants will float this year – SpaceX, perhaps, at 4 – 5% – won’t reverse the long-term decline on their own.

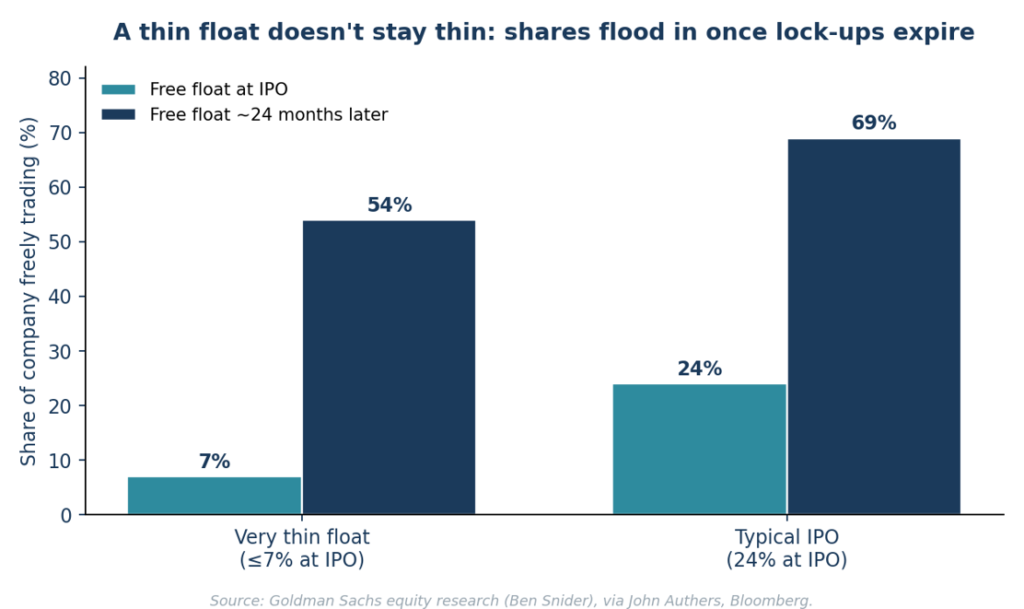

The catch is timing — and thin floats do not stay thin. Goldman’s work shows that big companies floating 7% or less of their stock have 54% trading within two years; across the IPOs it studied, a 24% float at debut became 69% within 24 months. As founder lockups expire, the supply withheld at the IPO finally hits the market.

A thin float doesn’t stay thin: the share of a company freely trading roughly two years after listing. Source: Goldman Sachs equity research (Ben Snider), via John Authers, Bloomberg.

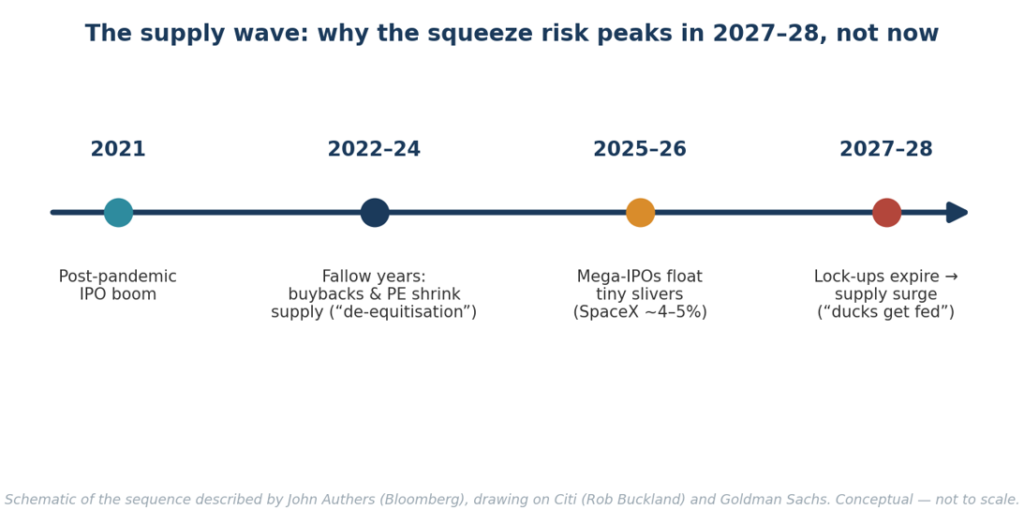

History rhymes: in the dot-com cycle, IPOs peaked in 1999, and the market topped and broke in 2000, as lockups ended and founders cashed out. Buckland himself now argues, in the FT, that the de-equitisation “put” is fading in the US: “in US big-cap tech, [the ducks] have been quacking for some time… It finally looks like they are about to be fed.” That points to the squeeze risk peaking not today, but plausibly in 2027–28.

The likely sequence: thin floats now, a heavier supply wave as lockups expire. Schematic, after John Authers (Bloomberg), drawing on Citi and Goldman Sachs. Conceptual — not to scale.

For our clients, the conclusion is the one our structure already delivers. Fundamental weighting means we are not forced to buy these names at inflated prices on day one. And our active asset-allocation overlay means that if and when the supply wave makes markets fragile, we can step back – hold more cash and lower-risk assets – rather than be dragged along.

There is also a governance dimension Authers and Matt Levine both flag: founders such as Musk intend to keep near-total control, so new shareholders “come along for the ride” without a meaningful say, and passive funds risk being used as a vehicle to absorb stock at whatever price the benchmark dictates. Real economic substance – not hype, and not the hope of influence – is what earns a place in your portfolio.

Blockchain and “tokenised” listings

“Tokenisation” means representing a share, fund or other asset as a digital token on a blockchain ledger rather than through conventional registrar-and-custodian plumbing. In principle, it can make settlement faster and cheaper — the legitimate case for it.

The danger is in the marketing: tokens promoted as “asset-backed” by property or by stakes in exciting pre-IPO companies, where the backing assets are illiquid, hard to value, or simply not what they are claimed to be. A recent example was the SEC enforcement action against Unicoin, which trumpeted “$3 billion in sales” of supposedly asset-backed tokens, even though its own audited accounts showed it had raised at most $110m. It is an old trick — magic beans in new technology.

Our portfolios invest only in regulated, listed, liquid instruments — mainstream UCITS ETFs and the like. We do not hold crypto tokens, tokenised pre-IPO stakes or “asset-backed” digital currencies of this sort and have no intention of doing so. We watch it closely as a market-structure development, but it is not a route through which client capital is exposed.

The bottom line

The risks are real, but they land on the passive investor who is structurally forced to buy whatever the crowd has bid up. Our portfolios are built on the opposite principle: fundamental weighting that ties holdings to companies’ real economics rather than their share prices, an active overlay that lets us manage risk when markets turn, and a strict diet of regulated, liquid instruments that keeps the tokenisation circus well away from client capital.

Alan Miller

Chief Investment Officer

Important information

The value of investments can go down as well as up, so you could get back less than you invest. Past performance is not a guide to future returns. SCM Private does not give personal advice based on your circumstances; we aim to provide understandable information so investors can make fully informed decisions. If you are unsure about the suitability of our portfolios, please contact an independent financial adviser. Charts marked “illustrative” are conceptual and are not forecasts or representations of any specific holding. SCM Direct is a trading name of SCM Private LLP, authorised and regulated by the Financial Conduct Authority (No. 497525).