A SCM Direct view on the Pensions Commission’s May 2026 interim report.

A diagnosis everyone in our industry has been making for years

The Pensions Commission’s interim report, published on 19 May 2026, has been described as a long-overdue “wake-up call.” The blunter description is that “We are already in a pensions crisis”.

The Commission’s headline numbers are sobering:

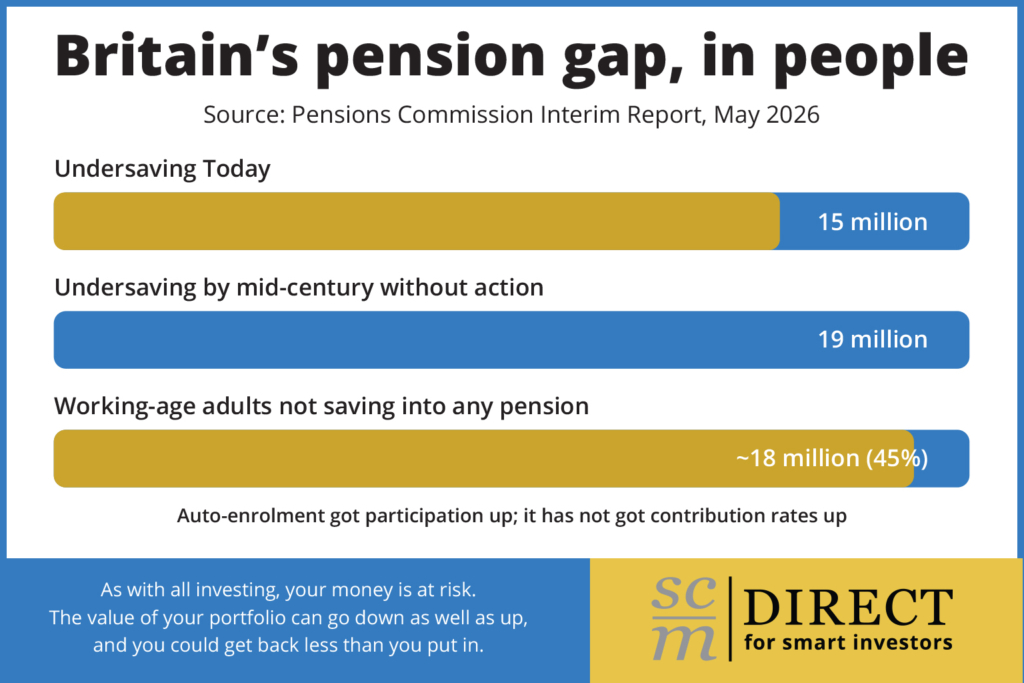

- Around 15 million people in the UK are currently under-saving for retirement, rising to 19 million on the current trajectory.

- Approximately 18 million working-age adults (roughly 45%) are not saving into any pension at all.

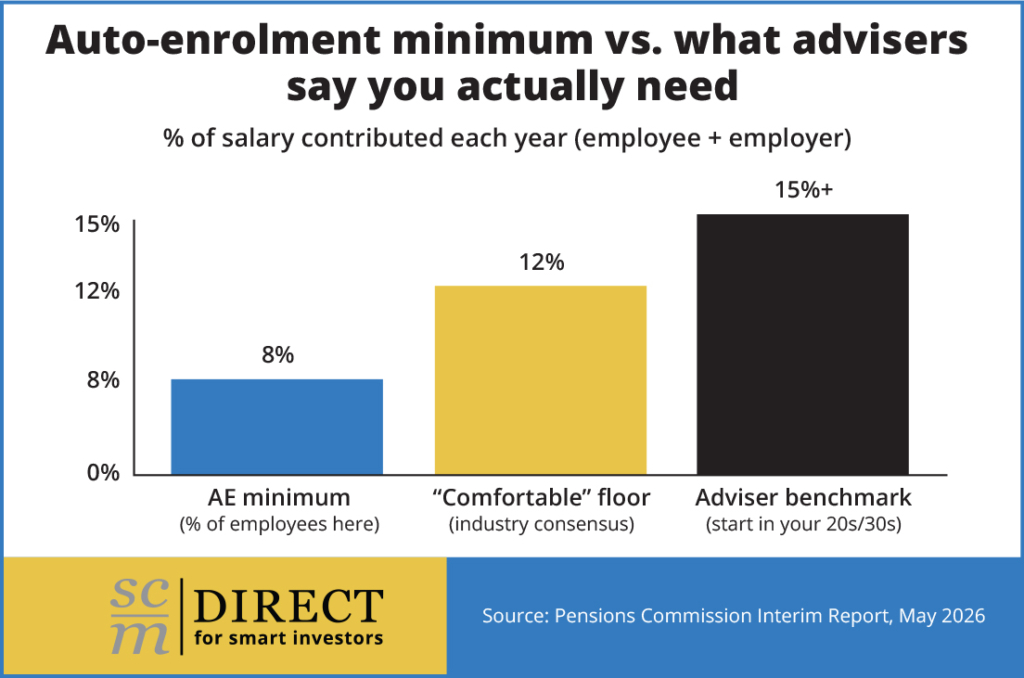

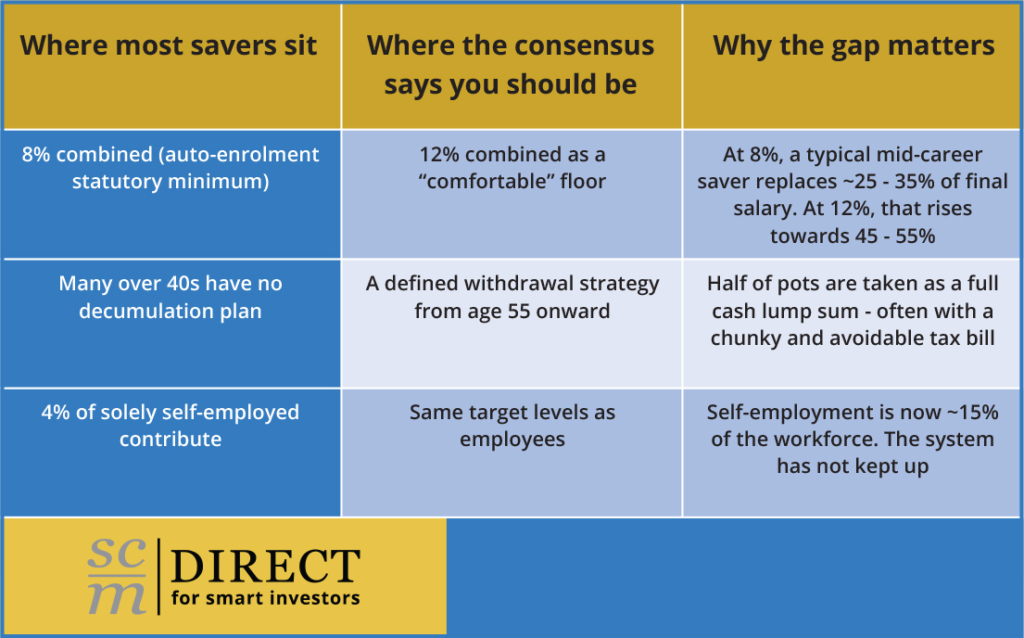

- About three-quarters of employees who do save are contributing less than 12% of their salary, the level most retirement adequacy studies treat as a floor for a comfortable later life.

- Only around 4% of those whose income is solely from self-employment are paying into a pension.

The “depth challenge” the Commission was set up to confront is that auto-enrolment fixed participation, but it has not fixed adequacy. Default contribution rates of 8% combined (employee + employer) were never going to deliver the lifestyle most savers picture when they hear the word “retirement”. They were a foothold, not a destination.

Why this matters more than most market headlines

Investors spend a remarkable amount of time worrying about things they cannot control – central bank decisions, geopolitics, the next inflation print – and far less time on the single financial variable that overwhelmingly determines their later life: the percentage of their income they save, and the cost-efficiency of the wrapper they save it in.

Consider the arithmetic that the Commission is asking the country to face up to.

Contribution rate is the lever, not investment performance

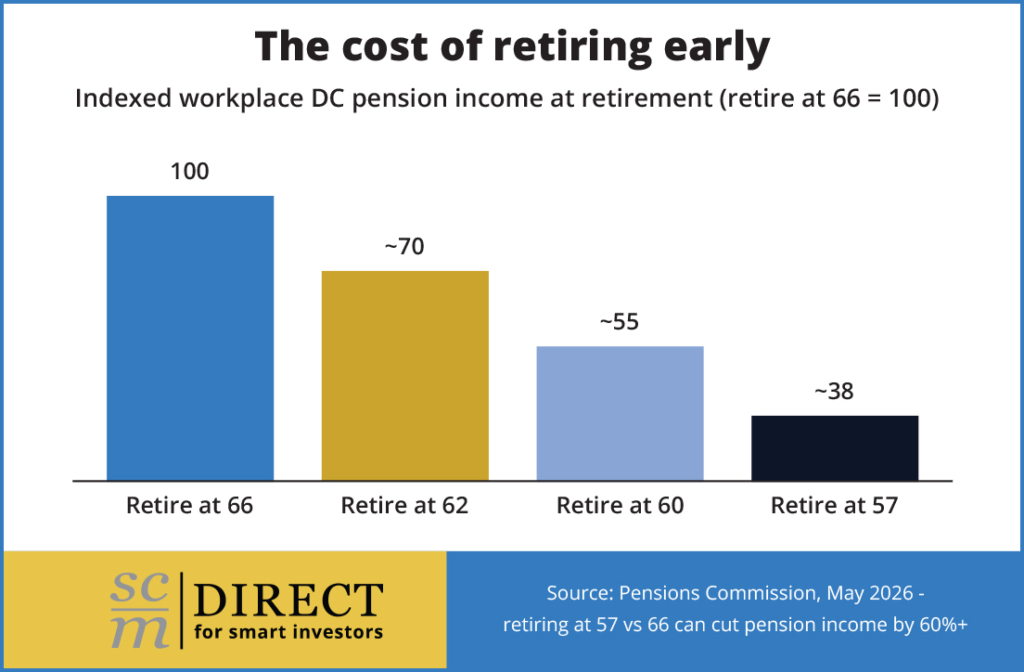

If you want to retire early, the cost is bigger than people think

Aiming to retire say 9 years early, 57 instead of 66, can mechanically reduce pension income by more than 60%. Fewer contributing years, more drawing years, less compounding, and an earlier start on sequence-of-returns risk. Even a four-year early retirement (62 vs 66) typically costs around 30% of income.

That isn’t an argument against early retirement. It is an argument for funding early retirement properly, well in advance, rather than discovering at 56 that the numbers don’t work.

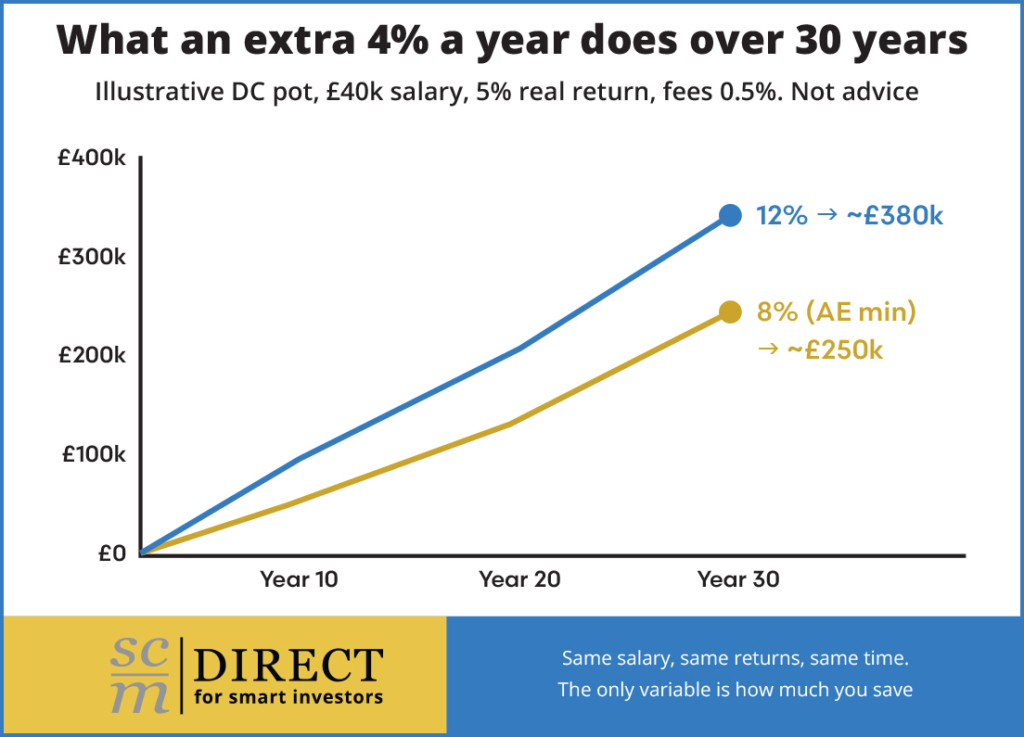

The effect of compounding – of a few extra percentage points

The story the chart below tells is the only story in retirement saving worth telling: contribution rate, time, and cost compound. Nobody can guarantee returns, but you can control how much they put in, and where.

Likely policy changes

Policy changes are likely to be slow. The Commission’s final report isn’t due until spring 2027, and ministers have already signalled that any meaningful legislative reform will be a matter for a future Parliament. We expect the eventual menu to include:

- A staged increase in minimum auto-enrolment contributions, very probably toward 12% combined.

- Removing the £10,000 earnings trigger and the lower earnings limit, drawing in more part-time and lower-paid workers (disproportionately women).

- A meaningful framework for the self-employed – likely default opt-in via the tax return.

- A new push on decumulation defaults so savers aren’t left to navigate drawdown alone at 60.

WARNING: These are all sensible. None of them will arrive in time to help anyone currently within fifteen years of retirement.

What you can do today to address any future pension gap

This is where the policy debate ends, and personal action begins. None of the following is novel, but all of it is being underused.

- Establish your actual retirement number – Most people quote a number they’ve read in a newspaper. Build your own: target income in today’s money, multiplied by a sustainable withdrawal rate (often 3.5 – 4% for a 30-year retirement), less State Pension, less DB income. The shortfall is the figure your DC and SIPP assets need to fund. Without this number, every other decision is guesswork.

- Move your contribution rate towards 15% – Eight per cent is a floor; 12% is a base case; 15% across employee and employer contributions, starting in your mid-30s, is what gets most professionals to a “comfortable” retirement on standard adequacy benchmarks. If your employer matches, max the match before doing anything else – it’s the closest thing to free money in personal finance.

- Consolidate, but consolidate carefully – The average UK worker will have eleven employers in their career. Multiple small pots, multiple charging structures, multiple sets of paperwork. Consolidation into a transparent, low-cost SIPP often reduces total costs and gives you a single view of your retirement. Always check for safeguarded benefits (DB transfers, guaranteed annuity rates) before moving.

- Mind the fees – they compound too – A 1% difference in annual charges over a 30-year working life can reduce the final pot by roughly 25%. This is one of the few elements of retirement outcome that is entirely within the saver’s control, and it is consistently under-managed. Demand transparency on platform fees, fund fees, transaction costs, and adviser charges.

- Plan decumulation 10 years before you decumulate – Building the pot is the easy half. Drawing it down tax-efficiently, in the right order across ISAs, GIAs and pensions, and at a sustainable rate, is the hard half. The Commission’s data – half of pots taken as cash, three quarters of over-40s with no plan – is what happens when this stage is left to the last minute.

Don’t be blasé, pay attention to pensions

The phrase “pensions crisis” gets thrown around so often it has lost meaning. The Pensions Commission’s interim report is useful precisely because it is dispassionate.

The diagnosis is structural: a system designed for an era when most people retired from one employer on a defined-benefit pension is being asked to deliver retirement for a DC, multi-employer, gig-economy workforce. So, it is inevitable that there is a gap.

The crisis isn’t really about the system. It is about the 15 million people inside it who are quietly assuming someone, somewhere, has done the maths on their behalf. No one has!

The good news is that the maths is fixable on an individual basis. The earlier and more honestly you face it, the cheaper it is to fix.

Take action

If you’d like to see what a low-cost, transparent SIPP looks like to avoid a retirement gap, we’d encourage you to start here:

Capital at risk. The value of investments can go down as well as up. Tax treatment depends on individual circumstances and may change in future. This article is intended as general information and does not constitute personal financial advice.