As you might naturally expect, we keep a close eye on our competitors and funds that are similar to our various portfolio strategies.

For many years, I have been cynical of the performance of many Absolute Return Funds that produce precious little returns for investors. What is also mystifying is why advisers are sending clients hard earned money to this sector despite the dismal performance. The Investment Association (IA) Targeted Absolute Return sector was the best-selling sector in June with net retail sales of £445m; with net retail sales for the asset class having risen by £333m year-on-year since June 2014.

“Survival of the fittest” is a phrase that originated from Darwinian evolutionary theory as a way of describing the mechanism of natural selection. This does not seem to apply to the IA Targeted Absolute Return sector, which appears to operate on the adage “survival of the fattest” in terms of huge fees, often including performance fees.

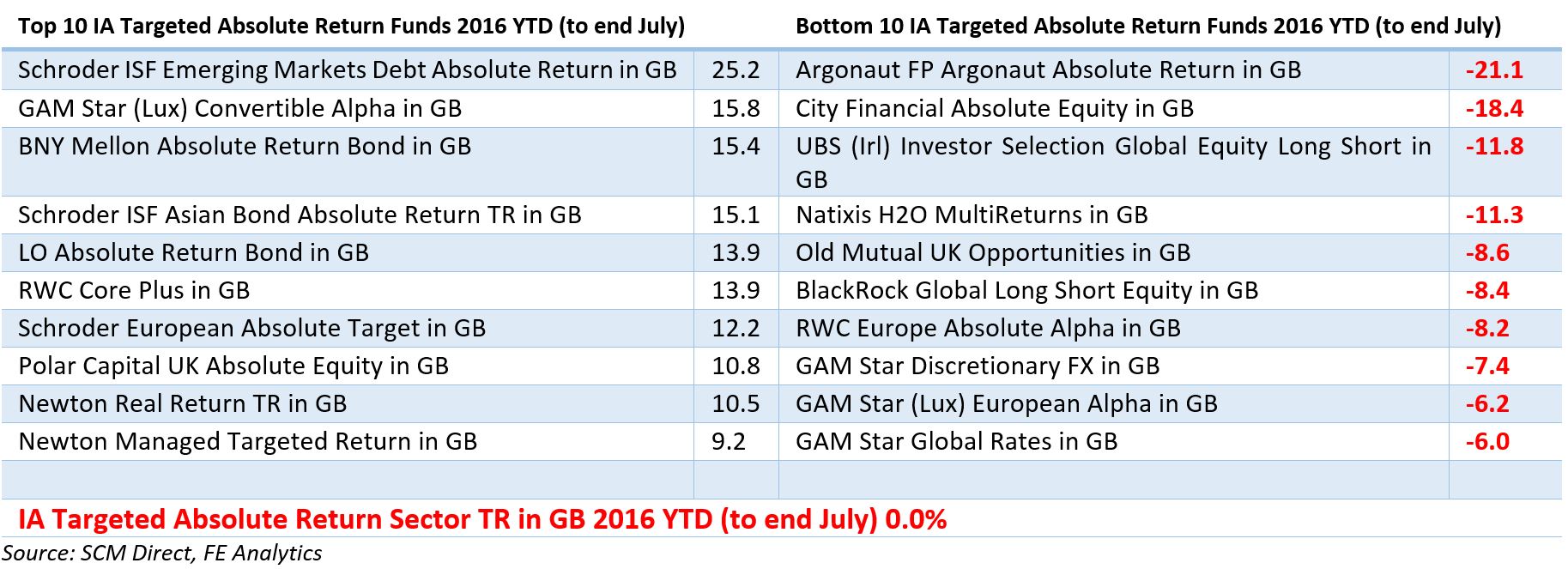

I looked at performance to the end of last month (end July 2016) to see whether the performance of these retail funds was less shockingly bad than usual. The IA Targeted Absolute Return sector has achieved a return of precisely 0% in 2016 – to the end of July, with the below showing the best and worst returns so far:

Looking at the bottom three funds, they seemed to have taken a significant Brexit hit. One of these is a conventional long/short equities fund concentrating mainly in UK equities, which fell 8.6% in June, another is long/short portfolio with significant exposure to small and medium sized companies which fell 12.7% in June.

They are not alone, the sector giant, the Standard Life Global Absolute Return Strategies Fund (GARS) – worth £26,840.7M as at 31/05/2016 – also suffered a Brexit hit and fell by 3% in June. The manager in a recent interview ascribed to being “caught off guard by Brexit and the surprising returns and dispersion of returns across the sectors“. He then talked about the realised volatility of the fund over one year as being just 5% compared to 14% for global equities. However, over the last 12 months to end July, the GARS fund fell by 4.8%, whilst global equities in sterling increased by 18.2% (MSCI World in GBP).

Is this the real issue with some of these funds? The fixation of some investors and advisers with volatility has made them forget about returns? Are some of these funds either too complicated for their own good or trying to eke out small individual returns to reduce risk, but when added up, these either cancel each other out or do not offset the various costs involved?

Another reasonable question is, how is it possible for some of these funds to lose so much in 2016 when virtually every single investable asset category apart from cash and UK small companies has risen between 3 and 26%?

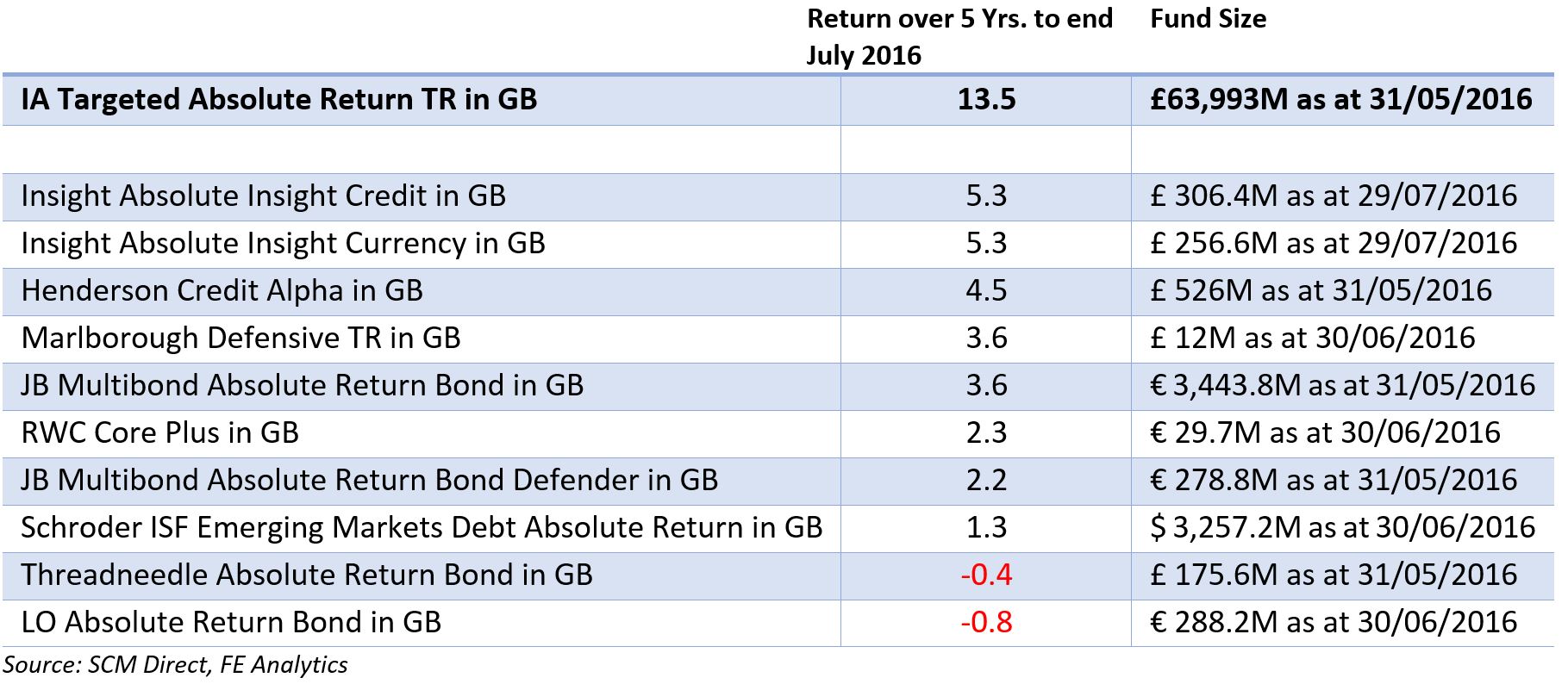

Of course, it is right to say you can’t judge a fund over such a short period, so here are the IA Targeted Absolute Return funds with the worst performance over the last 5 years to end July with Fund Sizes:

Since we started our SCM Absolute Return Portfolio in 2009, this is how it has fared against the average IA Targeted Absolute Return fund — see table below. Of course there are funds in the sector that have met their objectives and investors aspirations, but these are few and far between.

Conclusion

It seems to be that many fund group marketing departments are benefiting from the old adage that ‘bull**** baffles brains’ to allow their clients to forget the lousy performance of many funds.

Capital at Risk.

The value of investments can go down in value as well as up, so you could get back less than you invest.