If you thought COP26 was a COPOUT, with the inexcusable diluting of plans for ‘phasing out’ coal reduced to ‘phasing down coal’, there is equally inexcusable behaviour occurring in the aggressively promoted Ethical/ESG/SRI investing sector. (ESG = Environmental, Social, Governance and SRI = Socially responsible Investing)

When you look beyond the glossy brochures and green label of these funds, there is often extraordinarily little identifiable difference between the various Ethical/ESG/SRI funds and their closest non-Ethical/ESG/SRI comparisons. Ask most investors and they would assume any Ethical/ESG/SRI fund would be significantly different to the traditional non-ethical alternatives?

This blatant greenwashing is occurring in the UK investment and pension sector with little or no checks or action from the regulator or industry bodies, at the very time when investors, advisers and trustees are being told to actively direct investors to include Ethical/ESG/SRI funds in their portfolios. This is not just scandalous but makes a mockery of green investing and is allowing the exploitation of the very investors aiming to be prudent as well as environmentally and socially responsible.

SCM Direct did not seek to identify if providers were intentionally seeking to mislead investors but with few clear rules and regulations and data benchmarks of what definitions and constitutes an Ethical/ESG/SRI fund or stock, we find it hard for any organisation to justify selling these funds or labelling/classifying these funds as being ethical/SRI/sustainable given our research findings, and the ‘reasonable person’ test.

In the absence of any clear greenwashing rules or regulations, we would nevertheless highlight a fundamental FCA regulatory rule [1] that all communications should be ‘clear, fair and not misleading’. We strongly advocate the Boards of these Companies urgently meet with their compliance and marketing departments and decide whether these funds should (where appropriate) have Ethical/ESG/SRI labelling/classifications and whether claims within their literature should be removed and (where appropriate) they ask Morningstar and other rating agencies to exclude their fund from being classified as a ‘sustainable investment’.

We recommend the FCA writing to senior executives of these companies to discuss these findings. Should the FCA deem that important rules have been broken, they should officially name and fine the companies so that other companies are motivated to address greenwashing within their own companies. Continuing to ignore SCM’s research and research from other experts, suggests that both companies and the FCA are turning a blind eye to such practices and do not have the consumer protection as a core principle of their businesses or regulation. For example, in July we highlighted the Legal & General ESG China CNY ETF Bond ETF as a prime example of greenwashing, but it is still being sold as an ESG fund.

Another highly effective, quick, and easy recommendation is for the FCA to introduce a rule on transparency of holdings (which has been law in the US since 2004 and has afforded US investors significant protection over the last 17 years) so UK investors are treated the same as their US counterparts, by having sight of 100% of investment holding, published quarterly. This would afford investors access to information so they can make better and fully informed decisions.

The SCM Direct Research

- Classification of ‘Sustainable Investment Funds’

Morningstar is an excellent investment tool where investors can freely access numerous data and characteristics of funds.

One of the labels prominently displayed by Morningstar is the ‘Sustainable Investment’ strategy which is defined as ‘focusing on sustainability, impact, or environmental, social, and governance (ESG) factors in its prospectus or other regulatory filings. This classification does not measure how Morningstar rates the effectiveness of the fund’s sustainable strategy. Instead, it reflects the fund’s stated objectives.’

Using this fund filter to look at GBP currency, UK registered funds with a ‘Sustainable Investment’ focus and which were classified in one of the various Investment Association sectors, SCM Direct analysed the 343 funds that arose from this screening and found that 10% of these funds have a corporate sustainability score which was worse than the average of their peers.

We then further interrogated some of these funds, particularly the funds which fell into the Morningstar ‘Sustainable Investment’ category even when their fund label makes no mention of an Ethical/ESG/SRI focus.

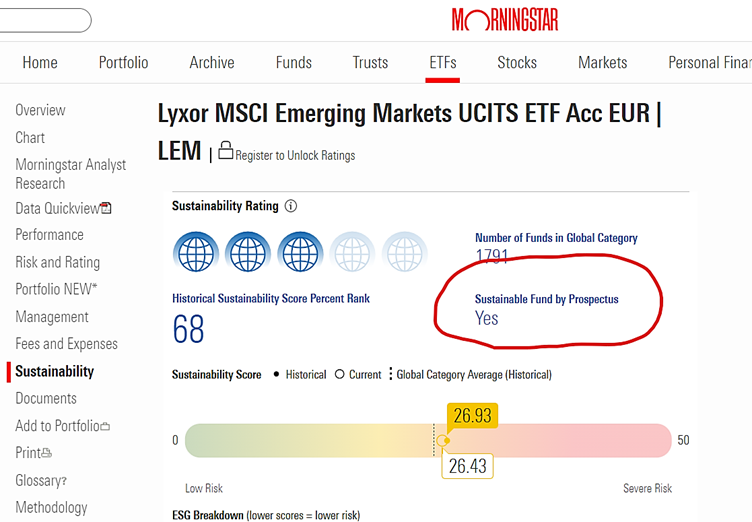

One such example is the Lyxor MSCI Emerging Markets ETF [2].

This fund is classified as a ‘Sustainable Investment’ Fund by Morningstar presumably because it mentions ESG in its prospectus but see the text highlighted in bold suggests this may not be appropriate:[3]

The Management Company aims to mitigate such sustainability risks by seeing to it that certain of its investment strategies exclude companies whose environmental, social and/or governance practices are considered to be controversial. A fund may further mitigate sustainability risks by adopting an ESG approach, inter alia, to its stock selection process or investment themes. Regardless of which method is used, there is no absolute assurance that all sustainability risks will be eliminated. More information on the integration of sustainability risks in investment decision-making processes can be found on the Management Company’s website at https://www.lyxor.com/investissement-socialement-responsable . Sustainability risks will not be a factor in the investment decisions of exchange-traded funds (ETFs), as these funds are either exposed to or directly invested in the components of an index.

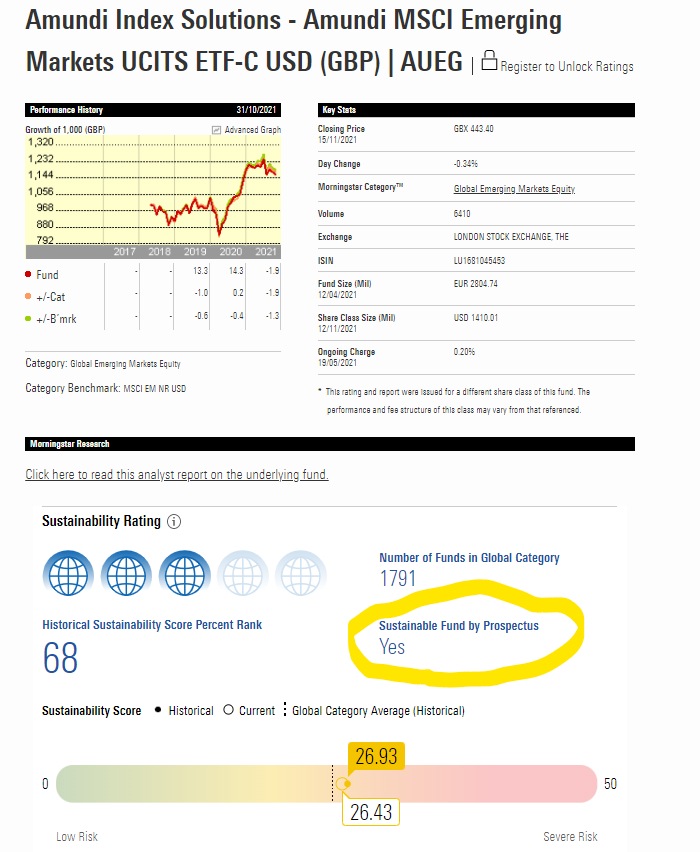

Another example is the £3.3 Bn Amundi MSCI Emerging Markets UCITS ETF, which is also a ‘sustainable investment’ according to Morningstar:

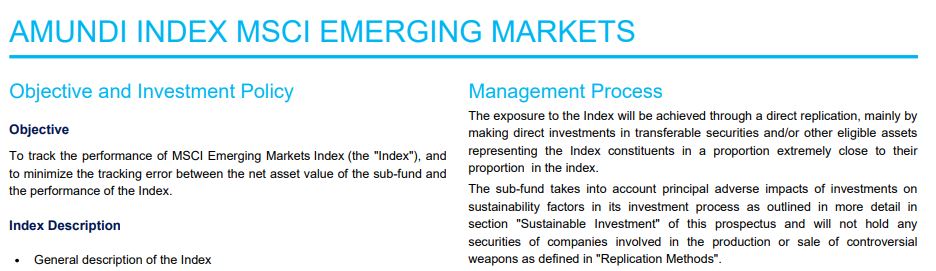

Again, this classification would seem to be due to its prospectus mentioning the incorporation of ‘sustainable investment’ but this seems to be limited to not holding controversial weapons stocks:

This begs the question, how many controversial weapons stocks exist in the world? Well, according to MSCI there are only 7 – given some of these companies are US (e.g. General Dynamics and Northrop Grumman), the impact of such restrictions on an Emerging Markets fund must be very small indeed:

The Vanguard SRI European Fund is labelled SRI by Vanguard [4] as:

‘The Fund promotes environmental and social characteristics by excluding companies from its portfolio based on the impact of their conduct or products on society and / or the environment. This is met by not holding stocks of companies in the Index that do not meet specific “socially responsible” criteria.’

‘The SRI screening process, which excludes Index constituents that are or have engaged in activities that result in serious violations of the UNGC, is consistent with the characteristics promoted by the Fund.’

‘The SRI screening process may also apply other criteria as necessary in developing the “socially responsible” screens, including avoidance of owning companies that are involved in, or are determined (by the Index provider) to derive revenues from, the production of controversial weapons such as cluster munitions, land mines, biochemical and nuclear weapons and those involved in the manufacture and distribution of tobacco products.’

‘The SRI screening process is a pre-determined, rules-based methodology applied objectively by the Index provider to the Index, which results in a SRI exclusion list of companies that have failed the screening process. The SRI exclusion list is then provided to the Investment Manager. The Investment Manager removes stocks of companies included in the SRI exclusion list from the list of Index stocks eligible for investment by the Fund.’

But what difference does this screening make in practice? The reality is that there is hardly any cluster munition, land mine, nuclear weapon manufacturers quoted so in practice its efforts seem to focus on a handful of stocks that represent a small portion of the market.

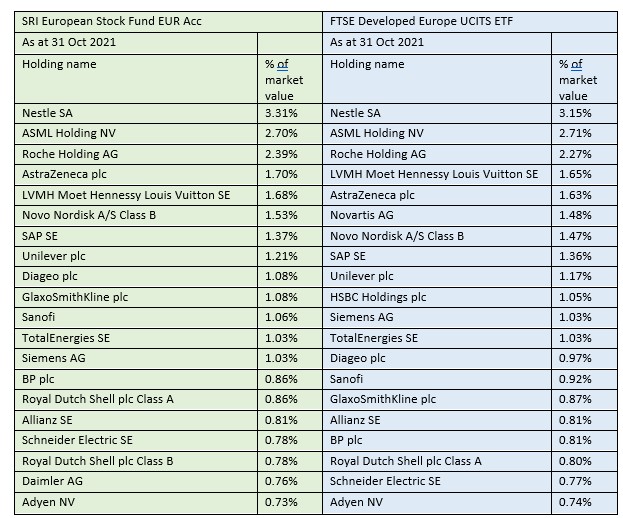

We compared the holdings of the Vanguard SRI European Stock Fund with Vanguards FTSE Developed Europe ETF based on the holdings on the 31st October 2021. The non-SRI fund holds 614 securities, of which we found only 25 were not in the SRI fund. The largest weightings of stocks within the Vanguard FTSE Developed Europe ETF, excluded within the Vanguard SRI European Stock Fund were Novartis (1.5%), HSBC (1.1%), BAT (0.7%), Airbus (0.6%), BHP (0.5%), Safran (0.4%), and Volkswagen (0.4%).

The differences are very small between the two funds weightings – we calculated the active share being just 9% which is exceptionally low indeed [5].

The Vanguard SRI European Stock Fund contained:

- 3 aerospace stocks (all with military exposure) – MTU, Saab, Meggitt

- 5 brewers – Anheuser-Busch InBev, Heineken, Carlsberg, Heineken Holdings, Royal Unibrew

- 1 building material stock that supplied the Grenfell Tower cladding – Kingspan

- 4 casino/gambling stocks – Flutter, Evolution, Entain, La Francaise des Jeux

- 2 copper producers – Antofagasta and KGHM Polska

- 1 defense company – Rheinmetall

- 5 general mining stocks – Rio Tinto, Anglo American, Boliden, Umicore, Imerys

- 2 gold miners – Polymetal International and Fresnillo

- 9 oil & gas stocks – Royal Dutch Shell A, Royal Dutch Shell B, Eni SPA, Equinor, Repsol, OMV, Galp Energia SGPS and Polskie Gornictwo Naftowe.

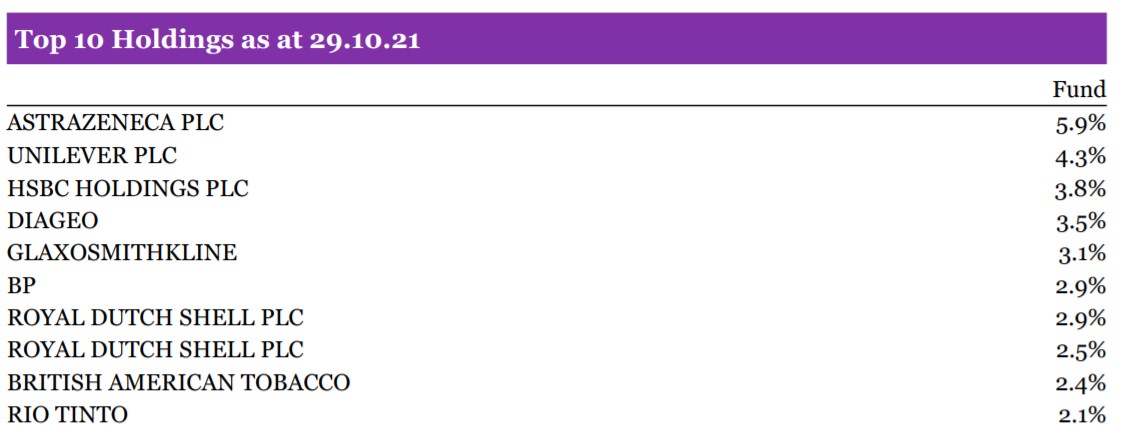

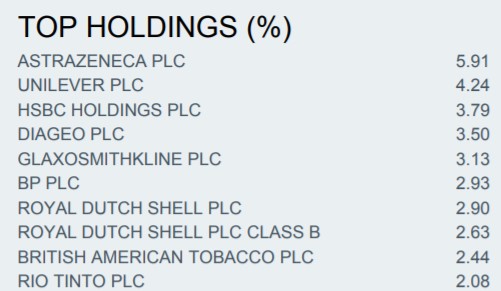

To see the similarity of the funds further, we looked at the top 20 holdings of each – the similarities were shocking to us:

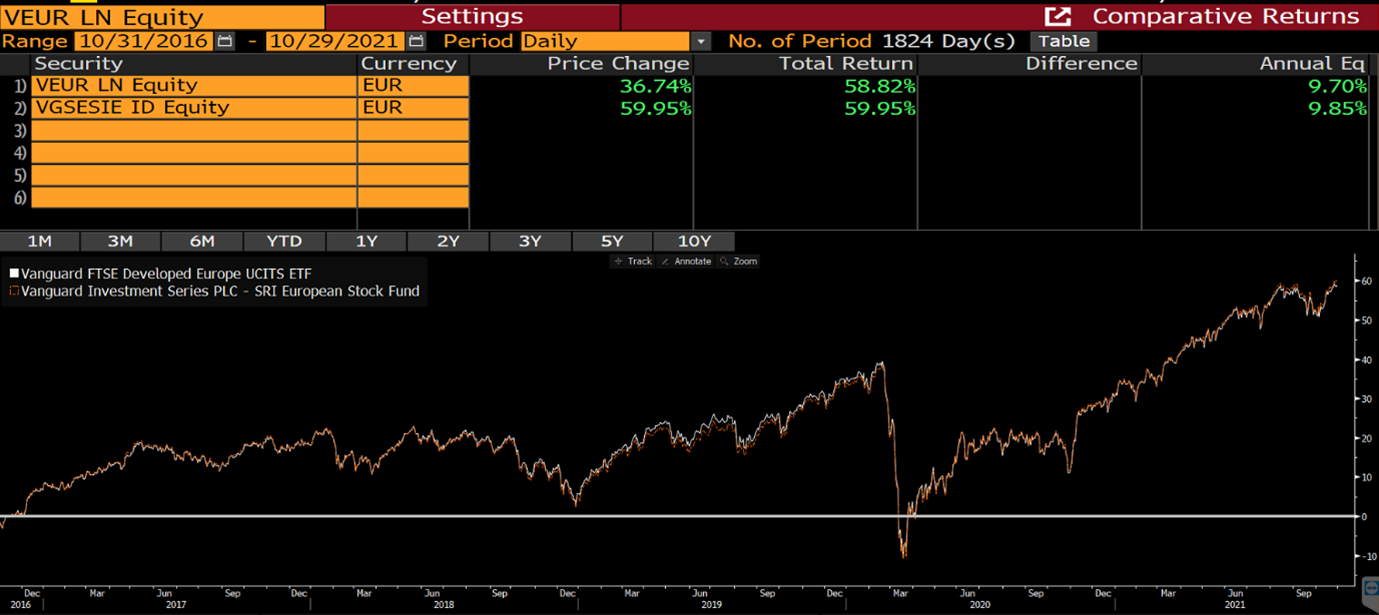

Given that the SRI fund is so close to the non-SRI fund in terms of its holdings and weightings, it’s not surprising the performance is practically the same:

Source: Bloomberg LP

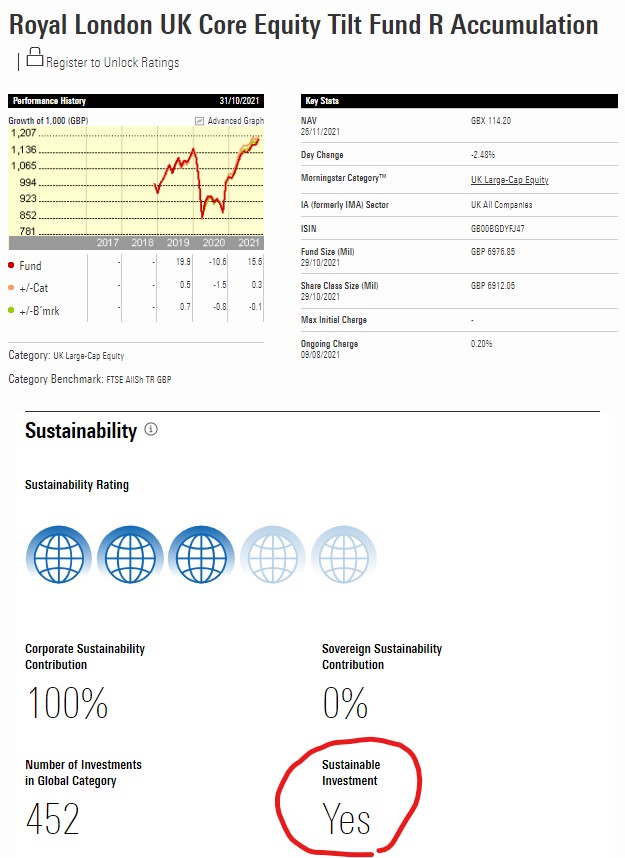

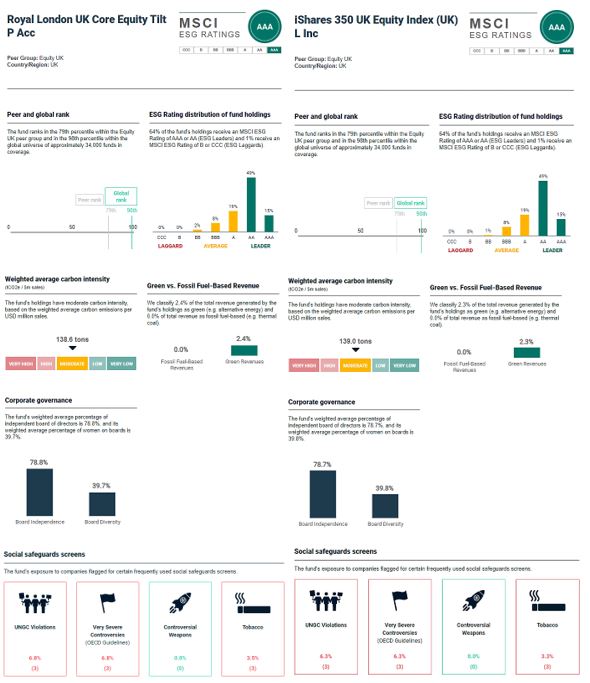

3. £7 BN ‘Royal London UK Core Equity Tilt Fund’

Morningstar says it is a ‘sustainable fund’:

This fund is classified as a sustainable investment fund by Morningstar, presumably due to it ‘incorporating responsible investment and environmental, social & governance insights into the investment process.’ And seeking ‘to achieve carbon intensity of at least 10% and up to 30% lower than that of the Index whilst also considering a company’s ability and willingness to transition and contribute to a lower carbon economy’.[6]

But when we looked at the performance of the fund, we found its performance was practically the same as the FTSE 350 Index, suggesting its ‘tilt’ did not amount to much:

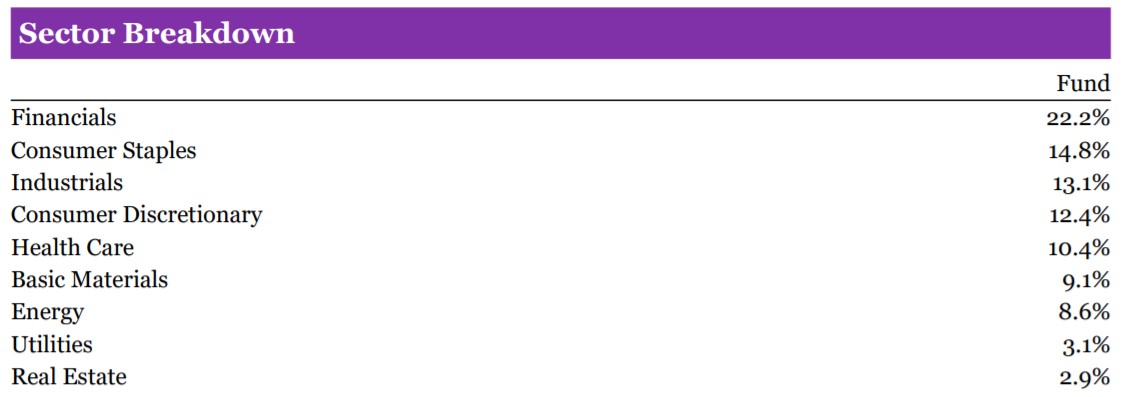

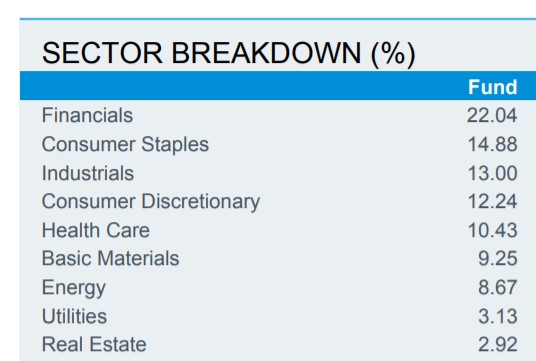

Top 10 holdings and sector weightings are remarkably similar to a FTSE 350 tracker (iShares 350 UK Equity Index Fund [7])

Royal London UK Core Equity Tilt Fund

iShares 350 UK Equity Index Fund

Royal London UK Core Equity Tilt Fund

iShares 350 UK Equity Index Fund

Given that the sector and stock weights are so similar, and it holds similar weightings in energy stocks, it seems unsurprising that based on MSCI data shown below, it fails miserably to achieve its objective of seeking ‘seeking ‘to achieve carbon intensity of at least 10% and up to 30% lower than that of the Index.

According to MSCI its carbon intensity is 138.7 tons [8] which is less than a 1% lower than the iShares FTSE 350 fund [9] – an exceptionally long, long way away from 10-30% which the fund ‘seeks’. In fact, it’s hard to see any evidence, based on the MSCI scores, of any ESG significance.

It is SCM Direct’s view that caveat emptor in the Ethical/ESG/SRI sector of pensions and investing, which is attracting billions, is not just scandalous and mis-selling, it is immoral, and the industry, regulator and Ministers must act now to clean up greenwashing.

[1] https://www.handbook.fca.org.uk/handbook/COBS/4/2.html

[2] https://www.morningstar.co.uk/uk/etf/snapshot/snapshot.aspx?id=0P0000M6YB&tab=6&InvestmentType=FE

[3] https://www.lyxoretf.co.uk/en/instit/resources/documents/prospectus/lyxor-msci-emerging-markets-ucits-etf-acc-usd-capi/fr0010435297/gbp?documentLanguage=English

[4] https://www.vanguardinvestor.co.uk/investments/vanguard-sri-european-stock-fund-gbp-acc

[5] https://www.investopedia.com/articles/mutualfund/07/active-share.asp

[6] https://documents.financialexpress.net/Literature/53FDCA16D047CA6E6DC6AEDAF69CC6D2/176880553.pdf

[7] https://www.ishares.com/uk/individual/en/literature/fact-sheet/ishares-350-uk-equity-index-fund-uk-class-l-dist-gbp-factsheet-gb00bcdpb465-gb-en-individual.pdf

[8] https://www.msci.com/our-solutions/esg-investing/esg-fund-ratings/funds/royal-london-uk-core-equity-tilt-p-acc/68558640

[9] https://www.msci.com/our-solutions/esg-investing/esg-fund-ratings/funds/ishares-350-uk-equity-index-uk-l-inc/68245281

Capital at Risk.

The value of investments can go down in value as well as up, so you could get back less than you invest.