The UK housing market has consistently been in the headlines in recent year due to house prices hitting record highs. However, predictions for 2023 and beyond suggest a fall in house prices due to factors such as escalating mortgage rates, diminishing affordability, and economic uncertainties.

In this blog, we delve into the detail with a comprehensive analysis of the UK housing market, examine various forecasts, and provide practical guidance for investors and homebuyers.

Background

Over the years, the UK housing market has experienced multiple cycles of growth and decline. Historically, it has served as a stable and profitable investment for both homeowners and investors, with house prices generally appreciating in the long run. However, the market has also experienced significant volatility, with steep price drops during economic downturns or housing bubbles.

Factors Affecting House Prices in 2023

Several factors are likely to influence the UK housing market in 2023 and beyond.

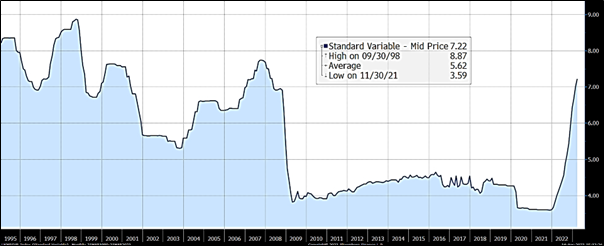

Mortgage rates: The Bank of England has raised interest rates multiple times in 2022, and the market is expecting further small rises in 2023. As borrowing becomes costlier, this exerts downward pressure on house prices. According to the Bank of England, variable mortgage rates have nearly doubled in the last 12 months:

Source: Bloomberg LP; Bank of England

Affordability: The combination of high house prices, low/stagnant wages, elevated debt levels, and rising cost of living has rendered homeownership increasingly unattainable for many. Reduced demand due to affordability concerns could contribute to a drop in house prices, with the Nationwide Building Society data showing the ratio of house prices to earnings, especially in London, has escalated from 5x to over 10x since late 2000.

Source: Nationwide Building Society

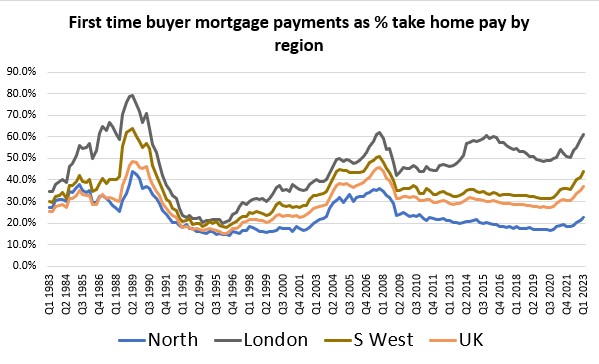

Mortgage payments for first-time buyers now constitute more than 60% of their net income in numerous UK regions, making it even harder for them to enter the market.

Source: Nationwide Building Society

Economic growth: The UK economy is forecasted to experience slower growth in 2023 compared to 2022. A sluggish economy could lead to job losses and diminished consumer confidence, adversely affecting house prices. The International Monetary Fund (IMF) predicts that the UK economy will contract by 0.3% in 2023 and then expand by 1% the following year.

External factors: The lingering negative economic effects of Brexit, surging inflation, and global events such as the war in Ukraine may contribute to economic instability and further impact the housing market.

House Price Forecasts

Several institutions have made predictions for the UK housing market in 2023 and 2024, including:

- Savills 10% decrease in 2023, 1% increase in 2024.

- Nationwide 5% decrease in 2023, 2% increase in 2024.

- Halifax 3% decrease in 2023, 1% increase in 2024.

- Capital Economics 5% decrease in 2023, 1% increase in 2024.

While these forecasts indicate a deceleration in house price growth or even a decline, actual changes could significantly deviate from these predictions due to various individual influencing factors.

Comparing Returns: Housing versus Shares in the UK

When comparing the returns of housing and shares in the UK, several factors, including historical performance, volatility, and the overall economic environment, must be considered.

Historical performance: Over the long term, both housing and shares have generally provided robust returns to investors. However, shares have historically outperformed housing in terms of average annual returns. The Barclays Equity Gilt Study reveals that the average annual return on UK equities from 1899 to 2021, adjusted for inflation, was approximately 5.3%, while the average annual real return for UK residential property stood at around 1.8% during the same period.

Volatility: Shares tend to exhibit higher volatility than housing, meaning their prices can fluctuate more rapidly. This can be both a positive and a negative, as it can lead to higher returns but also greater risk.

Government policy: The Conservative government have outlined policies such as introducing extra council tax on second homes and reforms to restrict homeowners Airbnb rentals. Plan would force Airbnb owners to seek planning permission before they can rent out their properties as holiday lets.

If Labour were in government, they would allow councils to charge a 300% council tax premium on properties empty for more than a year. Such policies could affect the housing market.

Overall economic environment: The overall economic environment can have a significant impact on the performance of both housing and shares. For example, during periods of economic growth, both assets tend to perform well. However, during periods of economic recession, both assets can experience losses.

As the chart below shows, for UK equities, their valuation (unlike housing) in terms of their estimate price/earnings ratio, is lower than the average of recent years:

Source: Bloomberg LP

Conclusion

The UK housing market is facing a number of headwinds in 2023, including rising interest rates, diminishing affordability, and economic uncertainty. As a result, it is likely that house price growth will slow or even decline in the coming year.

However, it is important to note that the housing market is cyclical, and there is always the potential for a rebound in prices in the future.

While housing has historically been a stable long-term investment, the current outlook suggests that shares may offer better short-term returns for those willing to take on higher risk. But ultimately, the decision to invest in housing or shares depends on individual circumstances, investment goals, and risk tolerance.

A smart, balanced approach is to include both asset classes to help diversify risk and provide exposure to different market dynamics, potentially enhancing overall investment returns.

Capital at Risk.

The value of investments can go down in value as well as up, so you could get back less than you invest. It is therefore important that you understand the past performance is not a guide to future returns. SCM Private does not give personal advice based on your circumstances. We aim to provide investors with understandable information so they can make fully informed decisions. If you are unsure about the suitability of our investment portfolios, please contact an independent financial adviser.

SCM Direct is a trading name of SCM Private LLP which is authorised and regulated by the Financial Conduct Authority to conduct investment business No. 497525.

SCM Private LLP is a limited liability partnership registered in England and Wales. No. OC342778