As 2019 begins with investment turbulence, existing and potential clients having seen recent major falls in stock markets have asked what our investment strategy for the year ahead is likely to be.

Here is our response in which we look back to our asset allocation decisions during the latter months of 2018 as well as consider what they are likely to be in 2019:

1. Many world markets were close to their highs in September 2018 and have now fallen back by between 9 – 15% from their end of August 2018 levels.

The table and chart below show the performance of the US S&P 500 index, the UK FTSE 100 Index, the FTSE Japan Index, the European STOXX 600 Index, and the global MSCI World Index from the end of August 2018 to the 3rd January 2019 close:

Source: Bloomberg

2. Our three core SCM Direct GBP portfolios have a mix of assets – how did these fare over the same period? With the asset spread / diversification within the portfolios, the bonds rose during the same time as equities fell, reducing the negative impact of the steep equity falls:

-

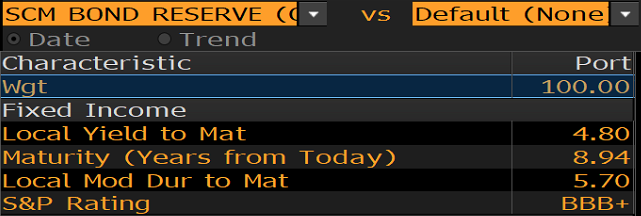

31st August 2018 – 3rd January 2019 close SCM Bond Reserve (GBP) +1.0%

SCM Absolute Return (GBP)

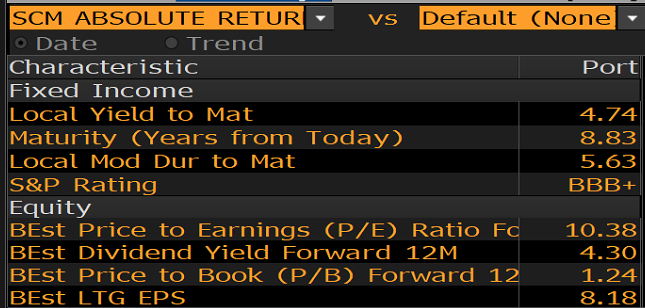

-5.7%

SCM Long-Term Return (GBP)

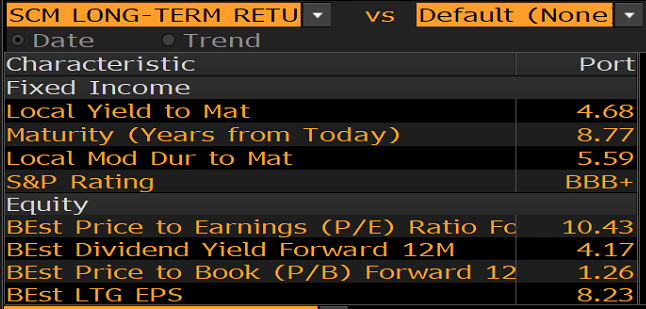

-8.0%

Past performance is not a guide to future performance. The value of the investment and the income deriving from it can go down as well as up and can’t be guaranteed. You may get back less than you invested. Rolling yearly performance available here.

3. The SCM Portfolios have fallen substantially less than these indexes due to the following factors:

i) They are not invested 100% in equities.

– The Bond Reserve Portfolio holds no equities

– The Absolute Return Portfolio was recently 60% invested in shares

– The Long-Term Return Portfolio was 74% invested in shares.

The bond element within the three portfolios has risen slightly over the period, particularly some of the ETFs held that are invested in emerging market local currency bonds (the top two ETFs):

Source: Bloomberg

ii) Sterling has fallen over this period, reducing the impact of some of the market falls within the GBP portfolios. For example, against the US$ it has fallen from about $1.30 to about $1.27:

Source: Bloomberg

iii) Within world stock markets, many of the severest falls have been in tech stocks. In early 2018 the decision to only be very lightly invested due to the findings of our fundamentals research that our team continuously undertake – particularly regarding US tech stocks.

The graph below shows that the NASDAQ index has fallen by 20% over the period, with many of the very largest US tech stocks falling by much more than this. Whilst most commentators are highlighting the dramatic 37% price fall of Apple, they are not alone. Amazon, Netflix and Facebook have all fallen by at least 25% over the same period:

Source: Bloomberg

iv) We actively made decisions to hold significant exposure to emerging market stocks that have, due to their much less demanding valuation, fallen much less during the recent market decline:

Source: Bloomberg

4. SCM investment strategy going into 2019:

i) Remain flexible and opportune to take advantage of market opportunities, which often follow sharp corrections.

For example, towards the very end of December we made substantial changes to our bond and equity holdings to take advantage of the recent weakness in the £ against the US$.

We switched many of the US$ denominated bond and equity holdings, wherever possible into GBP hedged versions as we believe going forward, Sterling is substantially undervalued, particularly against the US$. We have not hedged the Japanese Yen exposure as we believe the Yen is undervalued.

ii) We have focused more of the Portfolios towards “value” rather than “growth” stocks – again this has helped reduce the impact of the very steep market falls. The chart below shows how “value” stocks worldwide are now beginning to outperform “growth” stocks after many years of dismal performance:

Source: Bloomberg

However, even the recent return of value stocks has not made up for their dramatic underperformance over the last 5 years:

Source: Bloomberg

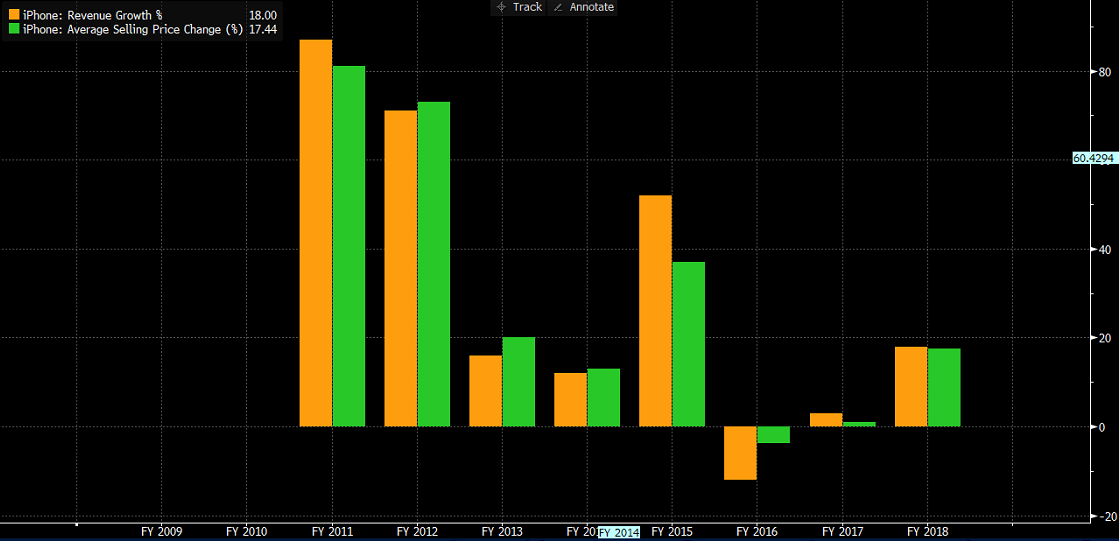

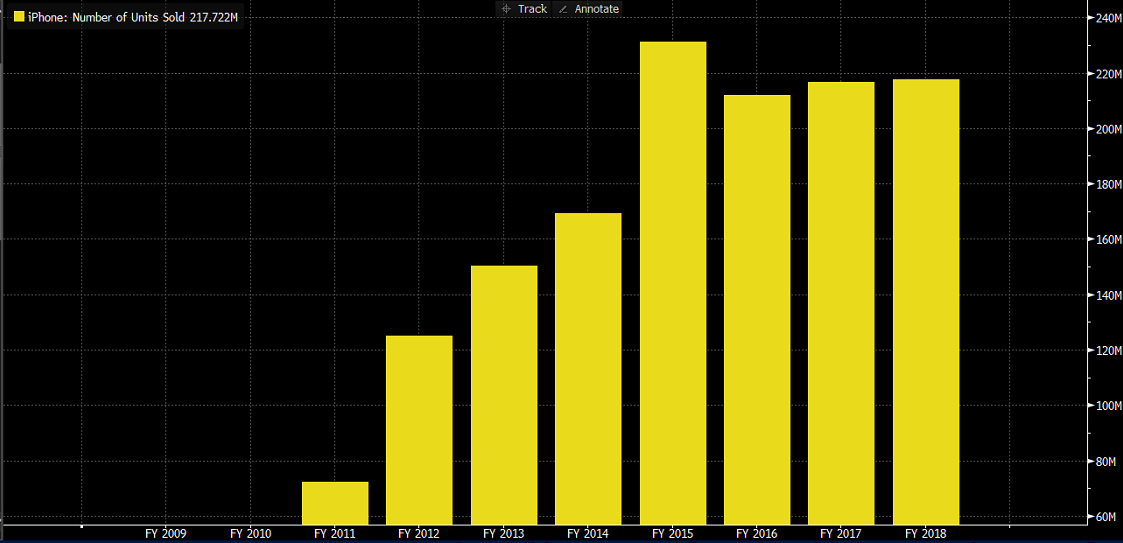

iii) We continue to focus on reducing individual stock risk – particularly of the more expensive tech stocks. For example, yesterday Apple warned about its outlook, leading to its shares falling by 10% as it cut its revenue forecasts for the first time in 16 years, blaming poor iPhone sales in China – as the charts below show, we believe the fundamental reason was not this at all.

We have been very nervous about tech stocks, including Apple, for some time as investors have been prepared to pay ever higher prices for this stock whose main engine, Apple iPhone has not seen volume growth in years (bottom chart), with revenue growth almost entirely based on ever increasing handset prices (top chart) which of course cannot last forever:

Source: Bloomberg

Contrary to the nonsense spouted by many active fund managers, you can invest via index funds without having to be exposed indiscriminately to the largest stocks, by being careful in selecting the strategies and regions in which the index fund invests.

SCM has been light in terms of US equities exposure and where invested, have focused on the “value” rather than “growth” or “tech” stocks. This has meant our exposure to shares in Apple represent under 0.2% of the SCM Long-Term Return GBP Portfolio and 0% of the SCM Absolute Return GBP Portfolio.

This compares to Apple’s weighting in the MSCI World index of approximately 1.9% after yesterday’s fall. Our SCM Portfolios do hold various Apple corporate bonds and floating rate notes, but these are backed by the fact that Apple holds cash of $130 bn at present.

The irony is that the so-called smart money within many leading hedge funds had significant exposure to Apple:

5. Is the glass half full or half empty?

The corollary of the sharp falls in markets over the last six months is that the fundamental valuations have fallen significantly, meaning that stocks are much more attractively priced.

The chart below shows the performance of global equities (MSCI World) versus the actual profits in terms of the earnings of the same stocks. You can see the yellow line for earnings shows that companies have reported strong growth in their profits but this has not been reflected in a higher share price – although of course there has been evidence of a slowdown in the US economy in December as the U.S. manufacturing PMI (Purchasing Managers Index) hit a 15-month low and over two thirds of manufacturers reporting higher costs, which they attributed to the rise in prices to tariffs.

Source: Bloomberg

Two of the other main worries highlighted by investors recently have been the continuing trade war between the US and China, and the prospect of higher interest rates in the US this year.

The irony is that the falls in markets recently and the economic and political pressures associated with such falls, make it more likely that the US/China trade talks will be successful – only a couple of days ago, the Chinese Caixin/Markit PMI (Purchasing Managers Index) slipped into contraction territory for the first time in 19 months.

The combination of falling markets, stocks e.g. Apple blaming China for their woes, and falling economic indicators e.g. the PMI, make it more likely that there will be some form of resolution.

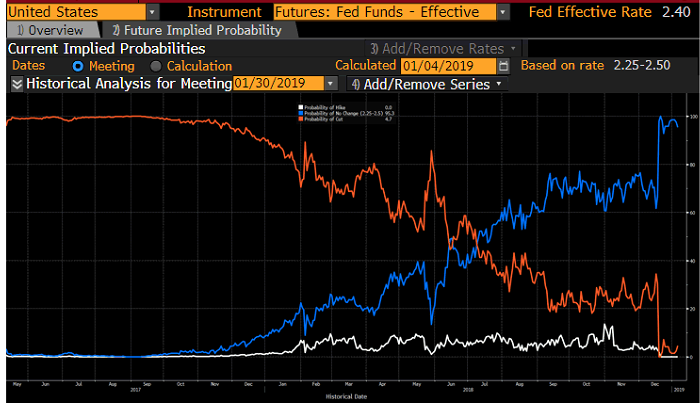

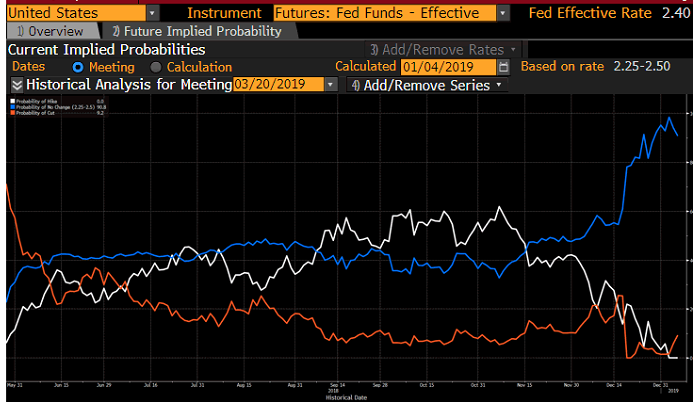

It also makes it less likely that interest rates in the US will rise substantially this year. As the chart below shows, the market implied probability of no change in interest rates (blue line) at the next Fed meeting at the end of January 2019 has risen to close to 100%:

Source: Bloomberg

Similarly, the probability of no change in interest rates (blue line) at the following Fed meeting on 20th March have risen to c. 90%:

Source: Bloomberg

6. The SCM portfolios continue to be widely diversified and the valuations of both the bonds and equities look compelling.

At present the bonds held within the GBP Portfolios are offering a yield (before all costs) of c. 4.7% or more per annum, whilst the shares held within the SCM Absolute Return and Long-Term Return Portfolios are growing their earnings by 8.2% pa and, are valued on just 10.4 x their prospective earnings with a prospective yield of 4.2% or more per annum (all figures reflect the valuation of the underlying holdings before any costs):

Source: Bloomberg

Source: Bloomberg

To put this into context against shares generally, the MSCI World Index that covers shares worldwide, is currently valued on 13.4 x prospective earnings with a prospective yield of 3% per annum.

The SCM Portfolio shares are therefore valued on a 22% discount in terms of their prospective P/E rating and a yield premium of about 40% (being 4.17%/2.97%).

Capital at Risk.

The value of investments can go down in value as well as up, so you could get back less than you invest.