No changes were made to the Portfolio in July.

Markets remained buoyant in July, with equities advancing again on the back of solid US economic data, resilient corporate earnings, and growing expectations that central banks, particularly the Federal Reserve, could begin easing policy. However, SCM remains sceptical that US rate cuts are as inevitable as markets seem to believe. This view is supported by fresh signs of inflationary pressure, particularly in tariff-sensitive sectors, and continued strength in activity data.

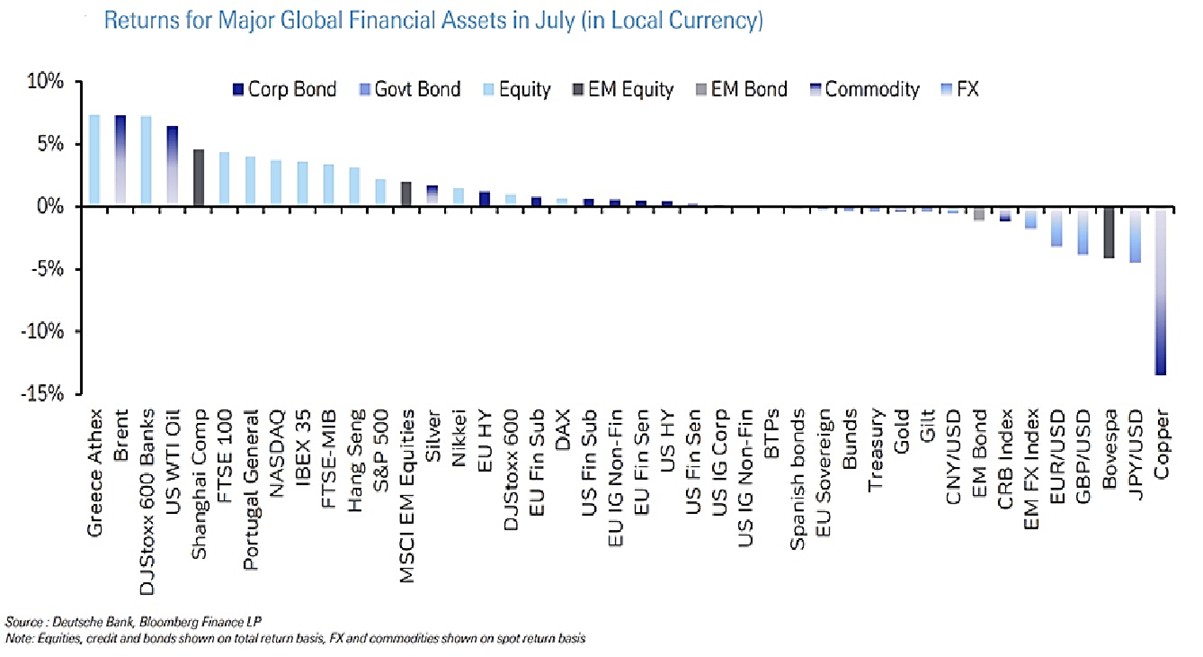

US equities posted further gains, led again by large-cap technology stocks. The Nasdaq registered 14 record highs during the month, with a narrow group of tech giants driving performance. Meanwhile, the US dollar rallied 3.2%, ending a six-month losing streak. The chart below shows asset performance across major global markets in July:

Tariffs Bite, and Inflation Lingers

President Trump’s evolving trade policy continued to dominated headlines. Several nations including Brazil, India, and Canada were hit with higher tariff rates, while others secured short-term extensions or agreed to revised deals. These moves coincided with the sharpest rise in goods prices since 2021, suggesting that tariff-related inflation may be starting to filter through to consumers. Despite political pressure, the Federal Reserve opted for a “hawkish hold” in July, and Chair Powell is expected to reinforce this stance.

SCM View: Market Optimism May Be Premature

Bond markets have priced in roughly 30 – 40 basis points of rate cuts by year-end, but we believe this confidence may be premature. The Fed faces limited justification for easing aggressively, particularly with inflation sticky and long-term fiscal concerns rising.

Market pricing in equities, particularly in the tech sector, increasingly reflects a one-sided view, leaving little room for error. Institutional investors have started to hedge against downside risk, with a noticeable uptick in demand for “disaster” puts on the Nasdaq 100. These highlights rising awareness of how stretched valuations have become in some parts of the market.

SCM Portfolios: Disciplined, Diversified, Cautious

Across SCM Portfolios, we remain focused on disciplined allocation. Equity exposure is diversified by geography and sector, with caution applied to areas showing excessive momentum or crowding. Our US equity position, which is currently unhedged, benefits from the recent dollar rebound. Fixed income allocations are concentrated in high-grade corporate bonds and UK and US Government bonds (our Ethical Portfolios do not hold government bonds). There is no exposure to high yield or EM sovereigns.

We believe the coming months will be shaped by three main forces: inflation persistence, central bank credibility, and earnings quality. As ever, SCM remains valuation-led and risk-aware.

Alan Miller, Chief Investment Officer

19 August 2025